New Starbucks CEO Not In Kansas Anymore

With North American traffic down -18% versus pre-pandemic levels, the beverage chain's issues (menu complexity, pricing architecture, customer service, China) will be no easy fix.

Yesterday afternoon, Starbucks (SBUX - $96.82) reported preliminary results for fiscal Q4 (FQE Sep 2024).

Next week, the company will officially report a fiscal Q4 comp store sales decline of -7% (US = -6% / China = -14%) with EPS of $0.80 (LY = $1.06).

The annual EPS for the just completed fiscal year appears to be in the neighborhood of $3.31, well below the company’s guidance range of flat to +LSD versus $3.54 LY (or, $3.54 to $3.65).

While a large-scale EPS decline relative to the prior management team’s guidance range, I’m not sure that matters today. I would not be surprised if the stock were to actually move higher today following yesterday’s preliminary earnings release.

On Monday evening, I published a note to clients suggesting a material lowering of go-forward top-line and bottom-line expectations was likely (see below). I think most savvy investors and analysts saw this coming.

When arriving just over a month ago, new CEO Brian Niccol likely told his finance team to (1) reverse what may have been a variety of accounting gimmickry that the previous management team was planning to utilize to achieve the stated $3.54 to $3.65 EPS guidance range and/or (2) accelerate expenses into fiscal Q4.

We’ll get a better sense of how this particular ‘sausage’ (Q4 earnings) was made when the company’s 10-K gets filed (mid-November 2024) via a review of various accruals and reserves.

But, from a bigger picture perspective, Mr. Niccol provided some initial thoughts on the company in the form of a video that the company posted to its IR website (in conjunction with yesterday’s press release).

In his video, Mr. Niccol suggested that “At Starbucks, coffee comes first.” That may be a reasonable starting point for the new CEO.

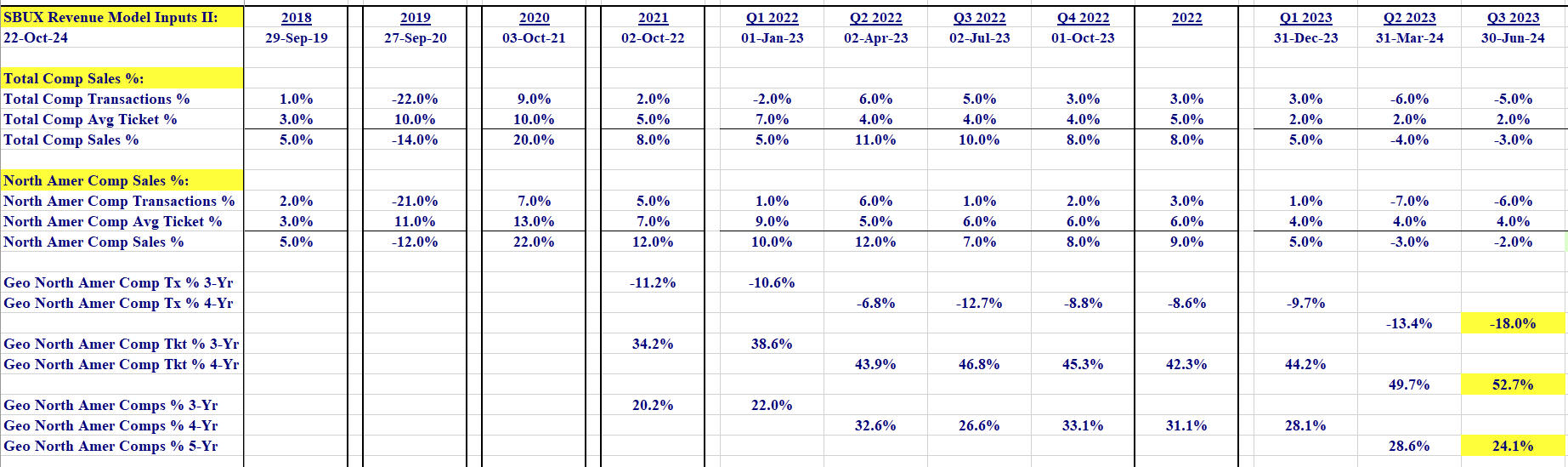

But, let’s be clear-eyed about this. The company’s success over the past 5+ years has been a function of driving average ticket higher. See below 5-year North American segment comp sales data.

In the June 2024 fiscal quarter, North American segment comp sales increased +24.1% over the past 5 years (i.e., compared to the June 2019 fiscal quarter… on a geometric basis).

The company has done a wonderful job being “all things, to all people.” Think incremental beverage platforms, cold beverages, drink customization, food attach. In the June 2024 fiscal quarter, North American average ticket was up +52.7% over the past 5 years.

Some of the above is discussed in this QSR Magazine article. See link below…

https://www.qsrmagazine.com/food/beverage/cold-drinks-now-represent-75-percent-of-starbucks-sales/

But, another material driver of average ticket growth has been pricing. While not formally disclosed by the company, I suspect that the average Starbucks customer no longer views the company as providing the ‘value’ it once did.

That may be the primary reason North American traffic is down -18.0% versus pre-pandemic levels (FQE June 2024). The reality is North American traffic dramatically declined in the first year of the pandemic and never recovered (and is now again headed lower).

Starbucks is no Chipotle Mexican Grill (CMG).

Under Mr. Niccol’s leadership, CMG did a wonderful job driving traffic with a consistent theme… a simple menu with higher-quality ingredients relative to peers in the fast-casual space and at a GREAT VALUE.

But, Mr. Niccol is not in Kansas anymore. Starbucks no longer has a simple menu and an argument could easily be made that the brand’s outsized price increases over the past 5+ years has driven customers to seek alternatives.

You may have noticed that we’ve not even discussed the company’s China conundrum yet. Or, the company’s ill-advised store growth. I’ll leave those topics for another day.

In closing, SBUX went out and found its rock star CEO (Niccol). He’ll get a long leash by the investment community. Also, he did a great job beginning to lower financial expectations yesterday.

But, let’s be clear… while Mr. Niccol says its “starts with the coffee,” the company’s largest issues (menu complexity, pricing architecture, customer service, China) will be challenging to solve and are likely to materially depress the company’s longer-term earnings power.

This is going to be fascinating to watch how this plays out over the next 2-3 years.